With the first round of funding completed and the second round underway, several businesses have received their Paycheck Protection Program loans from the SBA. This article will guide you through the rules that must be followed in order to gain maximum loan forgiveness as well as the rules that may reduce your forgiveness.

75% Rule

You must use at least 75% of the PPP funds on payroll over the 8-week loan forgiveness period to avoid reducing the loan forgiveness amount. This 8-week period begins on the date you receive the PPP funds, which may not necessarily be when you signed the loan agreement. Remember, payments to independent contractors cannot be included in the payroll costs. If you are having trouble reaching this 75% rule, you are allowed to increase employee salaries or wage rates, and even hire additional employees. Payroll costs includes the same additional expenses you used to qualify for funding when you first applied: insurance premiums, state and local payroll taxes, and retirement benefits.

Staff Retention Requirements

Another requirement to receive the maximum amount of forgiveness is to maintain the number of employees on payroll, specifically full-time equivalent FTE employees.

The number of FTE employees consists of full-time employees and part-time employees. Full-time employees are required to work at least 30 hours a week. For PT employees, combine all hours for the month and divide by 120. Add this number to FT employees to get total FTEs.

Below is an example on how to calculate your reduced forgiveness amount once you have done the FTE calculations.

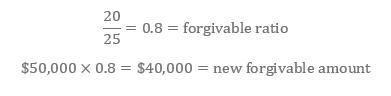

Bob’s Construction received a PPP loan of $50,000 on 5/1/20 and chose to have 20 FTE employees on staff on 6/1/20. On 2/1/20, pre-COVID-19 pandemic, the company had 25 FTE employees on staff. Since their company received a PPP loan and elected to have a 20% staff reduction in FTE’s, Bob’s Construction would then be responsible for repaying 20% of the PPP loan they’ve received.

*It is important to note that both the 75% rule and the staff retention requirements must be met to make the PPP loan 100% forgivable.

Staff Retention: Exemption

An exemption has been released for employees that were laid off or furloughed that decline a re-employment offer. These employees are not required to be included in the above calculations, assuming the following tests have been passed:

- A written offer must have been made in good faith

- Documentation of the employee’s rejection is maintained

- The offer includes the same salary/wage and number of hours as before the employee was laid off or furloughed

Maintenance of Salary Levels

The forgiveness amount will further be reduced if an employee’s salary during the 8-week period is not at least 75% of their salary during the quarter just before the 8-week period (usually quarter 1). Additional clarification is expected to be published in the near future as the actual calculation is a little confusing: the earnings for an employee during the 8-week period is compared directly with the preceding quarter, which is roughly 12 weeks and will inherently lead to discrepancies. Most likely, average weekly or monthly salaries will be used to compare the two periods more equitably.

Self-Employed Individuals (Sole Props & Independent Contractors)

Because self-employed people do not pay themselves through a traditional payroll and may not have any employees, 8 weeks of 2019 average net profit is automatically forgiven as a replacement for lost profit. The rest of the funds are still required to be spent on other qualified expenses, discussed below.

25% Rule: Other Qualified PPP Expenses

Aside from payroll, the PPP funds can be used for other qualified operating expenses. These include mortgage interest, rent, and utilities. Self-employed individuals are also allowed to use the funds for these expenses, the only additional rule is that you took or could have taken the expenses as deductions on your prior year schedule C return. Even though these types of expenses are not given the same amount of attention as payroll costs, make sure you retain documentation of the expenses to prove that the funds were used appropriately.

FAQs

- What is my interest rate if my loan isn’t forgiven? 1.00% fixed rate.

- When is my loan due? 2 years.

- Can I pay my loan early? Yes, there are no prepayment penalties or fees.

- When do my payments start? 6 months from receiving the funds.

- Are there any tax consequences? Yes, expenses that were paid using PPP funds and forgiven will not be eligible as operating expenses in that year.

- Are prepayment expenses permitted? Any prepayment of expenses are not allocable for forgiveness.

This article is to help PPP recipients have a better understanding of how the loan forgiveness is calculated and share some of our client’s most frequently asked questions. We wish everyone well during these unprecedented times.